Exploring heterogeneity and asymmetries in transfer pricing: evidence from Finland

Published in International Tax and Public Finance, 2026

Abstract

This paper utilizes detailed transaction-destination-level data from Finland for years 2013-2019 to examine how multinational enterprises adjust transfer prices to shift profit from high tax countries to low tax countries. Employing a triple difference strategy that leverages variations in corporate income tax rates and affiliate owner-ship, I provide robust evidence that multinational enterprises underprice exports to low tax destinations. Additionally, my findings suggest that transfer pricing serves as a complementary channel of profit shifting, as firms more prone to other profit shifting mechanisms also underprice their exports more. Furthermore, I provide evidence that firms with more affiliates as well as firms with tax haven affiliates transfer misprice more. My results also suggest asymmetries: while there is clear evidence of transfer mispricing in exports to low tax destinations, there is no con-sistent evidence of transfer mispricing in imports.

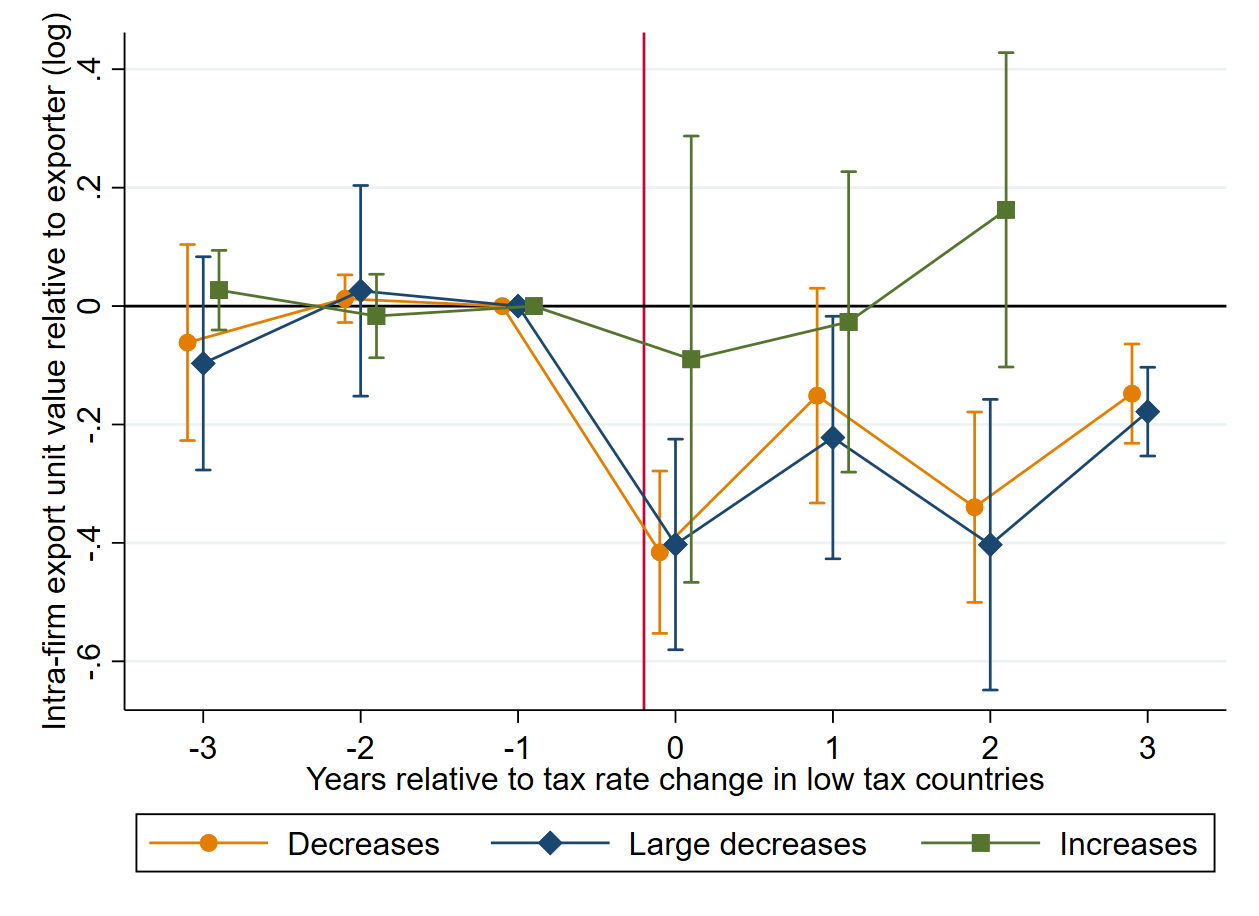

Effect of tax rate changes in low tax countries on the intra-firm export price

The figure plots event study estimates and the corresponding 95% confidence intervals for three different type of tax changes happening in year 0 in the low tax country. After the low tax country has decreased it’s corporate income tax rate (yellow and blue markers), the export unit value of a multinational that has an affiliate in that country decreases more compared to a firm that does not have any affiliates located in the country in question.

Recommended citation: Viertola, M. (2026), "Exploring heterogeneity and asymmetries in transfer pricing: evidence from Finland." International Tax and Public Finance.